Affinity Africa report lays bare the cost of Africa’s cash dependency – and the actions needed to break it

Accra and London, 17 June — Affinity Africa, Ghana’s leading digital banking platform, has released a new report in collaboration with the Mo Ibrahim Foundation and Yale’s International Leadership Centre examining the drivers and impacts of cash dependency in Africa and the steps required to address it.

The full report is available for download here.

The research makes clear that Africa’s cash dependency is not a technology problem. The continent already processes 74% of global mobile money volume — representing $1.1 trillion in value across 1.1 billion accounts in 2024. The problem is that digital payments do not yet outperform cash for merchants, households, and small businesses, resulting in more than 90% of mobile money value being withdrawn immediately upon receipt.

“The gap between the financial infrastructure Africa has built and the economic behaviour it was supposed to change is vast, and the cost of that gap compounds every year,” said Tarek Mouganie, Founder and Group CEO of Affinity Africa. “The problem is incentives. Digital payments do not yet outperform cash where it actually matters. Until digital is cheaper, more reliable, more accessible and more useful than cash at that level, the reality will not change”

The dependency on cash has significant economic consequences. Small and Medium Enterprises (SMEs), which account for roughly 80% of jobs and are often entirely cash-based, receive less than 5% of bank credit — contributing to a $330bn financing gap. Disproportionately high remittance fees, averaging 8.7% against the 3% SDG target, drain a further $8 billion annually from African households. Meanwhile, 85% of African workers remain in the informal sector, outside the tax base, limiting governments’ capacity to fund essential services.

“The SME financing gap, the annual remittance tax, the number of workers outside the formal economy — these are not inevitable features of the continent,” said Emma Sky OBE, Founding Director of Yale’s International Leadership Center. “They are the cost of an unfinished transition. Closing that gap is among the highest leverage moves available to anyone serious about Africa’s flourishing.”

The report makes clear that the issue can be addressed if the development of digital infrastructure is aligned with incentives, setting out three core actions that must happen together and in sequence — each creating the conditions for the next — to break cash dependency:

1. Make digital cheaper than cash for merchants: Regulators to cap merchant discount rates and provide fee subsidies for small merchants, while governments accelerate the shift by requiring digital payment acceptance for all government services, licences, and transfers.

2. Mandate interoperability: Regulators to mandate real-time settlement across platforms, enforce cross-border connectivity within regional economic blocs, and apply financial penalties for non-compliance.

3. Create reasons to stay digital: Regulators to give new digital innovators the headroom to offer credit, savings, and insurance products at scale; operators to provide transaction data as the basis for credit underwriting; and innovators to be given open APIs to build fintech products on existing payment rails.

Alongside the three core actions, the research also includes a detailed overview of the responsibilities of the other relevant stakeholders across Africa’s digital financial infrastructure – including governments, banks, Development Finance Institutions and investors – and the lessons that can be learnt from other markets in Africa and around the world.

“Incremental reform will not be enough. The public sector must move faster in building the regulatory clarity, institutional coordination, and governance frameworks capable of supporting Africa’s next phase of economic transformation,” said Mo Ibrahim, Founder and Chair of the Mo Ibrahim Foundation. “Because ultimately, ownership cannot exist without accountability, and economic autonomy cannot exist without strong institutions.”

The report calls actors to come together and address the issue as a matter of urgency. By 2050, one in four people in the world will be African — the window to get this right is narrowing, and the cost of incrementalism rises every year.

The full report is available for download here.

Media contacts: press@affinityafrica.com and will.king@thorndonpartners.com

About Affinity Africa

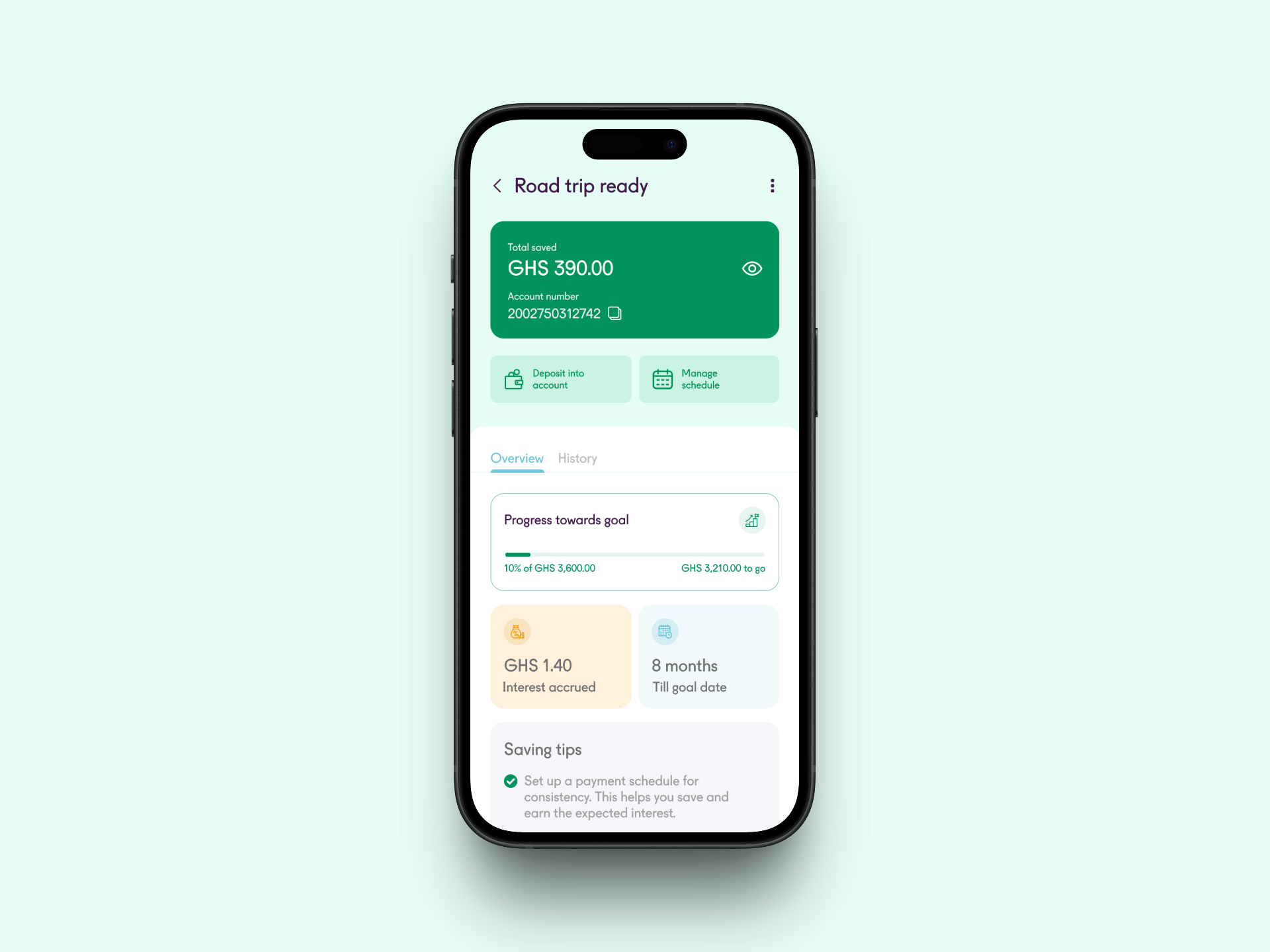

Affinity Africa is a digital banking platform founded by Tarek Mouganie and headquartered in Ghana, dedicated to providing affordable and accessible financial services to underserved and unbanked individuals, and micro, small, and medium enterprises (MSMEs). Powered by a proprietary technology platform, a branchless business model, and robust credit underwriting capabilities, Affinity offers 24/7 banking services tailored to both digital natives and users with limited digital literacy, driving financial inclusion at a low cost. Affinity is among the most affordable and cost-effective players in the region.

The company was founded in 2022, when it received a Savings and Loans license from the Bank of Ghana, the first of its kind granted in over 10 years, and officially launched operations in October 2024, following the regulatory approval of its mobile app. Today, it offers a comprehensive suite of products, including personal and SME accounts, savings, payments, transfers to banks and mobile money wallets, investments, and loans.

Affinity has made a profound impact in the region. It has empowered a large underserved population with easy-to-use affordable banking services, and it has financially included thousands of Africans into the system, who had been previously neglected by traditional banks: 65% of Affinity’s customers never had access to formal banking products and 60% are women operating in the informal sector.

To date, Affinity has raised US$13 million in total funding, including an US$8 million Seed Round, to support its mission to bridge the financial services gap across Sub Saharan Africa.

About the Mo Ibrahim Foundation

Founded in 2006, the Mo Ibrahim Foundation aims to amplify Africa’s voice on global issues, with a focus on the importance of governance and leadership. The Foundation provides data and analysis on the continent’s challenges, brings together key actors for discussion, and supports initiatives to improve leadership and governance.

In this regard, the Foundation concentrates on defining, assessing, and improving governance and leadership in Africa as key drivers of the continent’s progress. The Foundation places particular importance on African youth, recognising them as key actors in building their own continent. This goal is achieved through five key initiatives:

– Ibrahim Index of African Governance

– Ibrahim Prize for Achievement in African Leadership

– Ibrahim Governance Weekend

– Ibrahim Fellowships and Scholarships

– Now Generation Network.

About Yale’s International Leadership Centre

Yale’s International Leadership Center is an incubator and platform that develops and supports innovative, effective, and adaptive leaders to address the most acute and complex challenges facing the world. Located in Yale’s Jackson School of Global Affairs, the ILC facilitates the growth of leaders dedicated to preventing conflict and building better societies.

Through international competitions, the ILC identifies exceptional rising leaders from government, the private sector, and civil society, and provides them with opportunities to deepen and broaden their knowledge, skills, and networks and to access world-leading research, scholars, and practitioners.